Understanding Financial Literacy: A Beginner’s Guide to Managing Money

Financial literacy is essential for small business owners. It refers to the ability to understand and effectively use various financial skills, such as budgeting, investing, borrowing, and saving. In today’s complex financial environment, understanding these concepts can make a significant difference in the success of a business.

This guide will cover the importance of financial literacy and how it can help small business owners manage their finances better, including practical tips on banking, UPI systems, and digital banking.

What is Financial Literacy?

Financial literacy is the knowledge and understanding of basic financial concepts and how to apply them. For small business owners, this includes:

- Opening a bank account to save money and earn interest.

- Understanding inflation and the time value of money.

- Interpreting financial statements and making informed decisions based on them.

Importance of Financial Literacy for Small Businesses

1. Informed Decision-Making

Being financially literate helps business owners make better spending, saving, and investing decisions, leading to improved financial outcomes. This knowledge ensures that they can navigate through business challenges and capitalise on opportunities.

2. Budgeting and Planning

When creating a business plan, understanding budgeting is crucial. Financial literacy helps entrepreneurs develop a realistic budget, stick to it, and plan for future expenses. This ensures that they can manage finances effectively while staying within their means.

3. Debt Management

Understanding loans, credit, and interest rates helps avoid excessive debt and manage existing obligations. For example, knowing interest rates can help a business avoid high-interest loans, minimising financial stress.

4. Investment Knowledge

Knowing the basics of investment allows business owners to grow their wealth over time. Understanding where and how to invest can help them prepare for retirement, expand their business, or achieve other financial goals.

5. Risk Management

Financial literacy includes understanding insurance and risk management strategies. By being well-informed, businesses can protect their assets and mitigate potential losses through insurance policies and other safeguards.

6. Empowerment and Confidence

Being financially literate boosts confidence in managing finances. This empowerment allows small business owners to take control of their financial futures and make proactive decisions.

7. Business Sustainability

For small businesses, financial literacy is key to managing cash flow, expenses, and investments. These skills are critical for long-term success and growth.

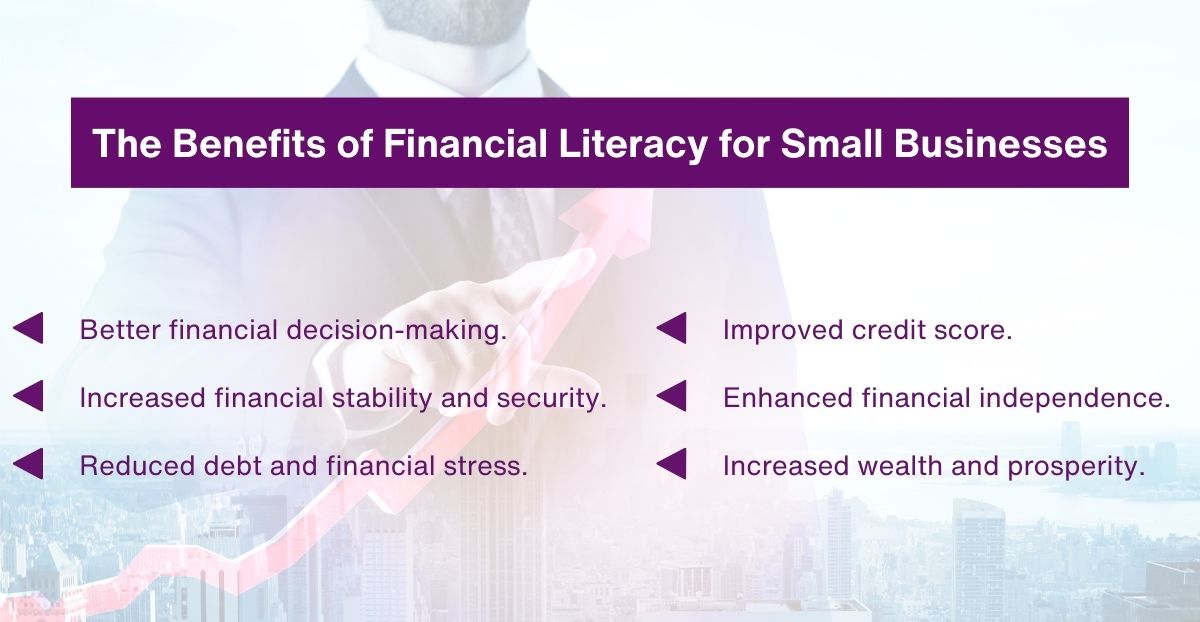

The Benefits of Financial Literacy for Small Businesses

- Better financial decision-making.

- Increased financial stability and security.

- Reduced debt and financial stress.

- Improved credit score.

- Enhanced financial independence.

- Increased wealth and prosperity.

Overall, financial literacy is crucial for achieving financial stability and fostering economic independence. It enables small businesses to thrive in a constantly changing financial landscape.

Types of Banking Accounts

Opening a bank account is one of the first steps in managing both personal and business finances. Depending on the needs, different types of accounts are available. Here’s a breakdown of some common account types:

1. Savings Account

A savings account is a deposit account where individuals can save money and earn interest on their deposits.

Key Features:

- Interest Earnings: You earn interest on the amount deposited.

- Limited Transactions: Generally, there are restrictions on the number of transactions per month.

- Types: Regular, salaried, children’s, senior citizens, women’s, institutional, and family savings accounts.

Ideal For: Individuals looking to save and earn interest on their deposits.

Example: PMJDY (Pradhan Mantri Jan Dhan Yojana)

PMJDY is a government scheme introduced in 2014 to provide no-cost savings accounts with zero balance requirements and additional benefits like insurance and overdraft facilities. This scheme has been instrumental in promoting financial inclusion, especially in rural areas, where 67% of accounts were opened. As of 2024, 56% of these accounts are held by women, showing the initiative’s impact on women’s empowerment.

2. Current Account

A current account is mainly for business owners, traders, and entrepreneurs, designed to handle frequent transactions.

Key Features:

- Overdraft Facility: Withdraw more than what’s available in your account.

- Unlimited Transactions: Ideal for businesses with high transaction volumes.

- No Interest: Unlike savings accounts, current accounts do not earn interest.

Ideal For: Businesses that need frequent transactions and easy access to funds.

In summary, while savings accounts are primarily for individuals aiming to save, current accounts are meant for businesses. Having a current account is a primary requirement for anyone looking to start a business, as it is necessary for applying for business loans or attracting investors.

Know Your Customer (KYC)

KYC (Know Your Customer) is a process used by banks and financial institutions to verify customer identities, ensuring security and compliance with regulations. It involves providing documentation such as:

- Proof of Identity: Passport, PAN card, Aadhaar card.

- Proof of Address: Utility bill, Aadhaar card, rental agreement.

- Photographs: Passport-size photos.

For partnership firms, additional documents like the partnership agreement and partners’ identity proofs are required.

Benefits of a Current Account for Entrepreneurs

A current account provides several benefits for business owners, including:

- High Security: Depositing cash in the bank lowers security risks associated with handling large sums of money.

- Business-friendly: With unlimited transactions, current accounts are designed to accommodate businesses with high transaction volumes.

- Overdraft Facility: This feature allows businesses to access extra funds during emergencies.

- Ease of Operation: Current accounts offer multiple options for transactions, including cash, cheque, and digital payments.

Charges on Current Accounts

Current accounts typically come with fees, including:

- Cheque bounce charges.

- Non-adherence to the minimum balance.

- Duplicate statement charges.

- Remittance charges (e.g., RTGS/NEFT/IMPS).

These charges may vary based on the bank’s policies.

Digital Banking and UPI

Digital banking has revolutionised the way businesses manage their finances. Today, most banking services are available 24/7 through online platforms and mobile apps.

Understanding UPI

UPI (Unified Payments Interface), launched by the National Payments Corporation of India in 2016, is a real-time payment system that enables instant transfers between bank accounts via mobile apps.

Why Use UPI?

- Single app for multiple accounts.

- Hassle-free online payments.

- No transaction fees for most payments.

- Secure, two-factor authentication.

UPI is particularly beneficial for small businesses, allowing them to manage transactions round-the-clock. With the PMJDY scheme, small business owners can even use their digital transaction history as collateral for loans, making UPI a crucial tool for those without traditional financial statements.

Conclusion

Financial literacy is an invaluable tool for small business owners. From understanding banking and investment principles to leveraging UPI and digital banking platforms, being financially literate allows entrepreneurs to make informed decisions, manage their finances effectively, and ensure long-term success. By grasping these concepts, small businesses can navigate the complexities of modern finance, leading to greater financial stability and growth.

Ready to take control of your business finances? Explore deAsra’s range of services including GST registration, business loan assistance, and cash flow management support. We also provide free resources and guides to help you navigate the financial landscape. Visit our blog section for more insightful tips on growing and managing your business effectively. Start your journey towards financial success with deAsra today!

FAQs

1. What is financial literacy, and why is it important for small businesses?

Financial literacy refers to understanding and effectively using financial skills like budgeting, investing, saving, and borrowing. For small businesses, financial literacy is crucial because it helps owners make informed decisions, manage cash flow, reduce debt, and improve their financial stability, ultimately leading to long-term business growth.

2. How can a small business create an effective budget?

To create an effective budget, a small business should first assess its income and expenses. Then, allocate funds to essential business activities like inventory, salaries, and marketing while saving for future needs. Regularly reviewing and adjusting the budget ensures the business stays on track financially and avoids overspending.

3. What are the main types of bank accounts a small business should consider?

Small businesses typically use two main types of accounts: savings accounts for earning interest on deposits and current accounts for handling frequent transactions without earning interest. A current account is essential for managing daily transactions and accessing overdraft facilities when necessary.

4. How can financial literacy help small businesses with debt management?

Financial literacy equips small business owners with the knowledge to understand credit terms, interest rates, and repayment schedules. This understanding helps avoid taking on excessive debt and enables better planning to pay off loans, ultimately reducing financial stress and improving the business’s credit score.

5. What is UPI, and how can it benefit small businesses?

Unified Payments Interface (UPI) is an instant, real-time payment system that facilitates seamless money transfers. Small businesses benefit from UPI by receiving quick payments from customers, making bill payments, and handling transactions without the need for bank charges, making it a cost-effective solution for managing finances digitally.