Mahila Udyam Nidhi Scheme: Empowering Women Entrepreneurs with Financial Support

Did you know that only 14% of entrepreneurs in India are women? This highlights a significant gap in business ownership. To address this, the government has introduced various schemes to support women entrepreneurs. One such initiative is the Mahila Udyam Nidhi Scheme, which provides financial assistance to help women start and expand their businesses.

If you are a woman looking to establish or grow your business, this scheme could be the perfect opportunity for you. Let’s explore the details of the Mahila Udyam Nidhi Scheme and understand how it benefits women entrepreneurs.

What is the Mahila Udyam Nidhi Scheme?

The Mahila Udyam Nidhi Scheme is a financial initiative introduced by the Small Industrial Development Bank of India (SIDBI). It aims to provide loans to women entrepreneurs in manufacturing, production, and service-related businesses. Initially launched under Punjab National Bank’s guidance, the scheme has expanded to other banks, making it accessible to more women across India.

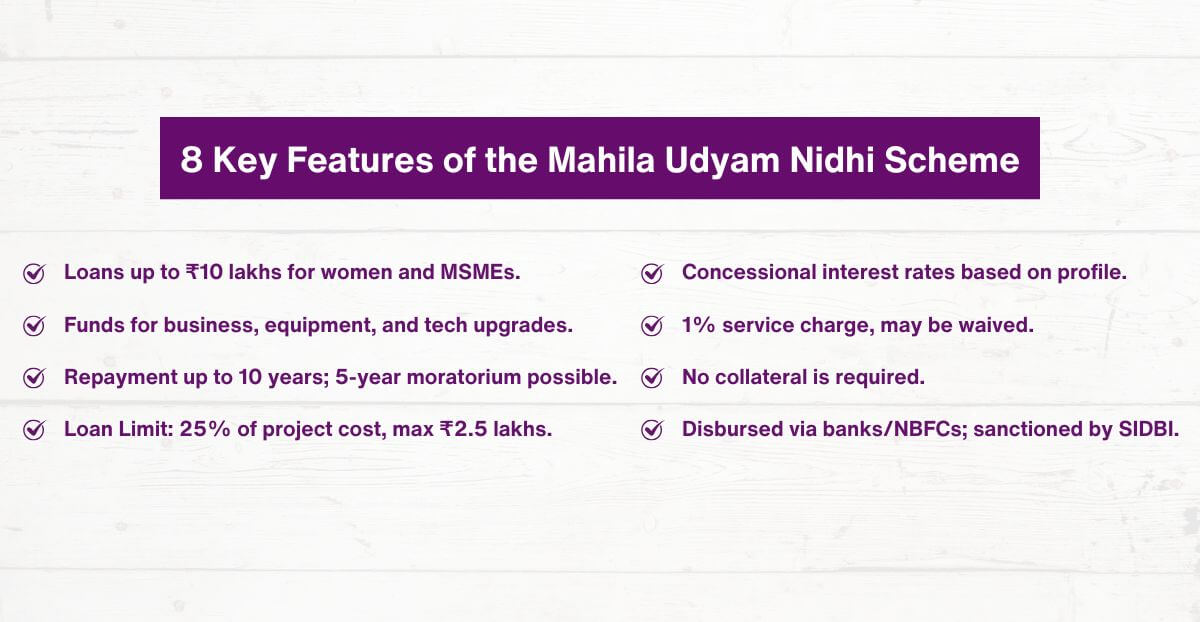

Features of the Mahila Udyam Nidhi Scheme

The scheme provides financial support through loans with favourable terms. Here are some key features:

- Loan amount: Women entrepreneurs and Micro, Small, and Medium Enterprises (MSMEs) can avail of loans up to ₹10 lakhs.

- Usage of loan: Funds can be used for manufacturing, production, and service-based businesses, as well as upgrading equipment and technology.

- Repayment period: The maximum repayment tenure is 10 years, with a possible moratorium period of up to 5 years.

- Loan limit: Women can avail of up to 25% of the total project cost, with a ceiling of ₹2.5 lakhs per project.

- Interest rates: Loans are provided at concessional interest rates, depending on the business type, project cost, and credit history.

- Service charges: A service charge of 1% per annum is applicable, with possible waivers at the discretion of the lending institution.

- Security requirement: No collateral is required for availing of loans under this scheme.

- Loan disbursement: The loan is sanctioned by SIDBI but disbursed through various banks, NBFCs, and microfinance institutions.

Mahila Udyam Nidhi Scheme Eligibility

To qualify for financial assistance under this scheme, applicants must meet specific criteria:

- Women entrepreneurs must own at least 51% of the financial holding in the business.

- Businesses should belong to manufacturing, production, service, or trading sectors.

- The business should have a minimum investment of ₹5 lakhs.

- The applicant should be engaged in business expansion, diversification, or technology upgradation.

- MSMEs, Tiny Units, or Small-Scale Industries (SSI) owned by women are eligible.

Approved Businesses Under the Scheme

The Mahila Udyam Nidhi Scheme supports various types of businesses, including:

- Beauty parlour

- Auto-repair and servicing centre

- Cyber cafe

- Tailoring business

- Laundry and dry cleaning

- Photocopying and desktop publishing

- Road transport operator

- ISD/STD booth

- Servicing agricultural and farm equipment

- Restaurants and canteens

- Mobile Repairing

- Crèche and daycare centres

- Typing and training institutes

Benefits of the Mahila Udyam Nidhi Scheme

The Mahila Udyam Nidhi Scheme is designed to make financial assistance accessible to women entrepreneurs. Some of its key benefits include:

- No collateral requirement, reducing financial risks for women.

- Lower interest rates, making borrowing more affordable.

- Flexible repayment tenure of up to 10 years, allowing for business stability.

- Encourages economic empowerment by increasing women’s participation in business.

- Creates employment opportunities by promoting small-scale businesses.

This scheme plays a crucial role in bridging the gender gap in entrepreneurship by providing women with the resources they need to succeed.

How to Apply for the Mahila Udyam Nidhi Scheme

Women entrepreneurs can follow these steps to apply:

- Visit the bank’s official website: Go to the Punjab National Bank (PNB) website or any other participating bank.

- Search for the scheme: Enter “Mahila Udyam Nidhi Scheme” in the search bar and proceed.

- Download the application form: Locate the MSME loan section and download the relevant form.

- Fill in business details: Provide details such as business type, investment amount, and financial projections.

- Attach required documents: Include proof of identity, business registration documents, PAN card, and contact details.

- Apply: Visit the nearest bank branch and submit the filled form with the necessary documents.

Government Support for Women Entrepreneurs

The Mahila Udyam Nidhi Scheme is just one of several government initiatives that support women-led businesses. The government also offers other financial and mentorship programs to encourage women to start and expand their ventures. Learn more about government support for women entrepreneurs here.

For more guidance on business planning and validation, check out our services.

Final Thoughts

The Mahila Udyam Nidhi Scheme provides women entrepreneurs with much-needed financial assistance and flexible repayment options. With government backing and simplified procedures, it is an excellent opportunity for women to establish and grow their businesses. If you are a woman entrepreneur, consider applying for this scheme and take a step toward financial independence and business success.

FAQs

1. What is the maximum loan amount available under the Mahila Udyam Nidhi Scheme?

Women entrepreneurs can avail of loans up to ₹10 lakh under the Mahila Udyam Nidhi Scheme. The amount can be used for business setup, expansion, or upgrading existing units.

2. Is collateral required for loans under the Mahila Udyam Nidhi Scheme?

No, this scheme does not require collateral or security. It provides financial assistance with flexible repayment terms, making it easier for women to access credit.

3. How long is the repayment period under this scheme?

The repayment period can be up to 10 years, with a moratorium period of up to 5 years. This flexibility helps women entrepreneurs manage their finances effectively.

4. Which banks offer loans under the Mahila Udyam Nidhi Scheme?

The scheme was initially launched by Punjab National Bank under SIDBI’s guidance. Now, multiple banks and financial institutions offer loans under this scheme.

5. What type of businesses are eligible for funding?

Businesses in manufacturing, production, and service sectors can apply. Approved activities include beauty parlours, tailoring units, mobile repair shops, and more.

DISCLAIMER:

This blog is provided by the deAsra Foundation (“deAsra”) for informational purposes only, offering insights that may be beneficial for micro, small, and medium-sized enterprises (MSMEs).

PLEASE NOTE: This blog is neither written nor endorsed by any governmental organization nor has any affiliation or connection with any government ministry in India. deAsra makes no warranty or representation regarding the information provided through this blog and disclaims its liabilities in respect thereof, including any liability for authenticity, errors, omissions, or inaccuracies in this blog, if any. Any action on the blog readers’ part based on the information provided in this blog is at his/her/its own risk and responsibility. deAsra reserves the right to modify the information contained in this blog at any time at its sole discretion. deAsra agrees that though all efforts have been made to ensure the veracity of the information in this blog, the same should not be construed as an accurate replacement for authorized commentary on the subject matter before it is used for any legal, financial, or business purposes. deAsra accepts no responsibility for the information’s accuracy, completeness, usefulness or otherwise. In no event will deAsra be liable for any loss, damage, liability, or expense incurred or suffered that is claimed to have resulted from the use or misuse of the information in this blog. We advise you to corroborate the information through authenticated sources and professional consultants before relying on the information stated in this blog. All the information in this blog is for educational and reference purposes only, and we do not make or charge any money to provide this information. Links to the relevant websites included in this blog are provided for readers’ convenience only. deAsra is not responsible for the contents or reliability of linked websites and does not necessarily endorse the views expressed therein. deAsra does not always guarantee the availability of such linked pages. If any content has been unintentionally published or copyrighted material in violation of the law, please don’t hesitate to contact us, and we will have it removed immediately