Pradhan Mantri Mudra Yojana: Empowering Small Businesses in India

Starting a small business in India can be daunting, especially when access to finance becomes a hurdle. For millions of budding entrepreneurs, turning ideas into thriving ventures requires initial capital that may not always be easy to obtain. This is where the Pradhan Mantri Mudra Yojana (PMMY) comes to the rescue.

Launched by the Government of India, this flagship scheme aims to empower micro and small enterprises by providing them with much-needed financial support. Through the scheme, businesses can secure loans up to ₹10 lakhs, fostering economic growth and entrepreneurship across the country.

What is Pradhan Mantri Mudra Yojana?

The Pradhan Mantri Mudra Yojana is designed to offer loans to small businesses that often face difficulties in obtaining credit from traditional financial institutions. The scheme caters to businesses in the non-farm sector, supporting enterprises engaged in manufacturing, trading, and services, as well as agriculture-related activities like poultry, dairy, and beekeeping. These loans are provided by Member Lending Institutions (MLIs), including public and private sector banks, non-banking financial companies (NBFCs), microfinance institutions (MFIs), and small finance banks (SFBs).

By providing affordable credit and ensuring easy access to finance, the scheme addresses a significant pain point for micro and small enterprises. The Pradhan Mantri Mudra Yojana ensures that small businesses can grow, thrive, and contribute to the nation’s economic progress without being weighed down by financial constraints.

Key Objectives of Pradhan Mantri Mudra Yojana

The Pradhan Mantri Mudra Yojana has a simple but powerful objective – to foster financial inclusion for small businesses in India. This scheme aims to:

- Provide collateral-free loans to micro and small enterprises.

- Encourage entrepreneurship among women, marginalised sections, and new entrants.

- Boost job creation by supporting small businesses in various sectors.

- Foster growth in India’s unorganised sector, which comprises millions of small enterprises.

- Facilitate easy and hassle-free credit to ensure business expansion and innovation.

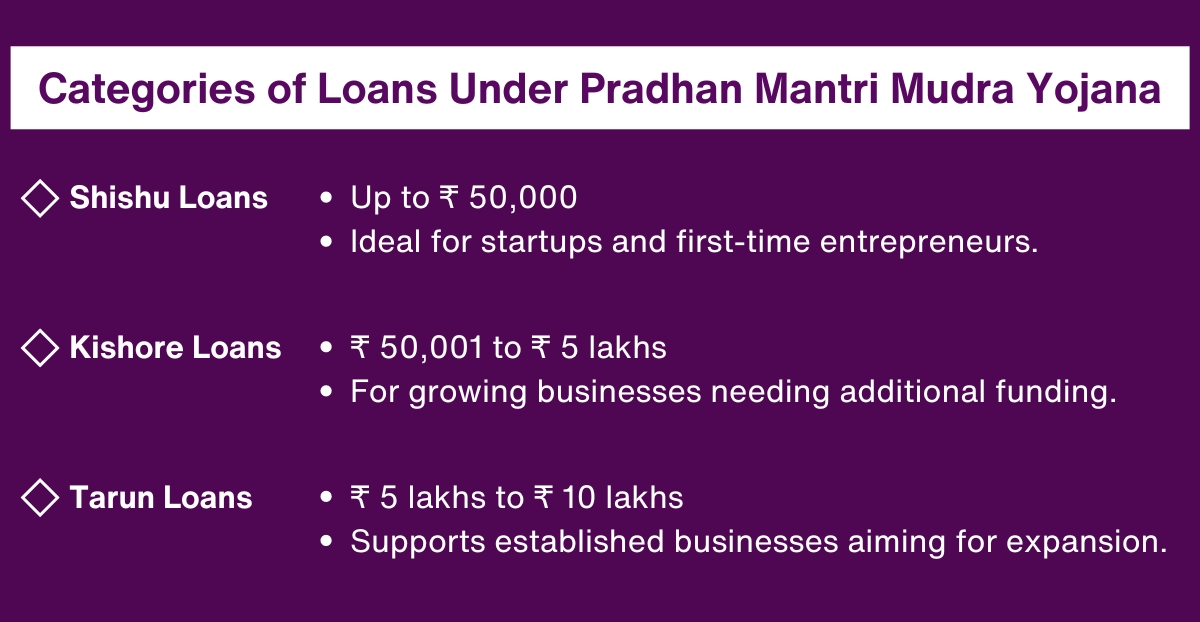

Categories of Loans Under Pradhan Mantri Mudra Yojana

The scheme has been structured into three distinct loan categories, which cater to the various stages of business development and the corresponding financial needs of the entrepreneur:

- Shishu Loans

This category is designed for businesses that are just starting. Under the Shishu category, loans of up to ₹50,000 are provided. It is particularly beneficial for first-time entrepreneurs who need an initial boost to get their businesses off the ground. - Kishore Loans

As businesses grow, their financial needs evolve. The Kishore loan category addresses this by offering loans ranging from ₹50,001 to ₹5 lakhs. Entrepreneurs who have started their ventures and need additional funding to scale can benefit from this category. - Tarun Loans

For well-established small businesses looking to expand further, the Tarun category offers loans ranging from ₹5 lakhs to ₹10 lakhs. This category supports businesses aiming to scale operations or diversify their offerings.

These three categories ensure that the Pradhan Mantri Mudra Yojana can support entrepreneurs at every stage of their business journey.

Eligibility for Pradhan Mantri Mudra Yojana

Understanding the eligibility for Pradhan Mantri Mudra Yojana is crucial for aspiring entrepreneurs who wish to apply. The scheme has flexible eligibility criteria to cater to a wide range of small businesses:

- Individuals, proprietary concerns, partnership firms, private limited companies, and public limited companies can apply.

- The business must be in the non-farm sector, such as manufacturing, trading, services, or allied agricultural activities.

- The applicant should not be a defaulter with any bank or financial institution and must have a satisfactory credit history.

- Educational qualifications are assessed based on the nature of the proposed activity, but formal qualifications are not a rigid requirement.

For entrepreneurs seeking guidance on whether they qualify, visiting platforms like deAsra Foundation can provide further clarity on the application process and support services available.

How to Apply for the Pradhan Mantri Mudra Yojana

Applying for a loan under Pradhan Mantri Mudra Yojana is a straightforward process. Entrepreneurs can visit the Udyamimitra portal or any Member Lending Institution to submit their application. Here’s a breakdown of the key steps:

- Online Application

Entrepreneurs can register online through the Udyamimitra portal by filling in personal and business details. Applicants will need to choose whether they are new entrepreneurs, existing entrepreneurs, or self-employed professionals. - Documentation

The following documents are required for the application:- Proof of identity (Aadhaar, PAN, Passport)

- Proof of address (Utility bills, rent agreement)

- Business-related documents (registration certificates, licenses)

- Financial statements (for Kishore and Tarun loans)

- Photographs (not older than 6 months)

- Submit the Application

Once all the details and documents are filled in and attached, the application is submitted. An application number is generated, which can be used for tracking the status of the loan application.

Practical Advice for Entrepreneurs

To increase the chances of a successful loan application under the Pradhan Mantri Mudra Yojana, entrepreneurs should consider the following tips:

- Prepare a Detailed Business Plan

Whether you are applying for a Shishu, Kishore, or Tarun loan, having a clear and well-documented business plan can strengthen your application. Include financial projections and show the viability of your business. - Maintain Good Credit

One of the key eligibility criteria is having a good credit record. Ensure that you have no defaults on existing loans, and maintain clean financial statements. - Choose the Right Category

Evaluate your current business stage and select the appropriate loan category. If you’re just starting, opt for the Shishu loan. The Kishore or Tarun loans are more suitable for businesses looking to scale.

For more information on government loan schemes for small businesses, you can check out this blog, which offers an overview of several such schemes.

Conclusion

The Pradhan Mantri Mudra Yojana is a game-changer for small businesses across India. By offering accessible, collateral-free loans, the scheme empowers entrepreneurs to overcome financial barriers and achieve their business dreams. Whether you are just starting with a Shishu loan or expanding your business with a Tarun loan, the PMMY is designed to meet the diverse needs of India’s thriving entrepreneurial community. The scheme provides a critical opportunity for those eligible to grow and contribute to the country’s economic progress.

Understanding the Pradhan Mantri Mudra Yojana and its application process is the first step towards unlocking the financial support you need to succeed. Make sure to explore your eligibility and take advantage of this impactful scheme.

FAQs

1. What is Pradhan Mantri Mudra Yojana (PMMY)?

The Pradhan Mantri Mudra Yojana (PMMY) is a government initiative launched to financially support small and micro-enterprises in India. It offers collateral-free loans up to ₹10 lakhs, aimed at businesses in the manufacturing, trading, and service sectors. The scheme empowers entrepreneurs by giving them access to affordable credit, helping them grow and sustain their ventures.

2. What are the different loan categories under PMMY?

The Pradhan Mantri Mudra Yojana offers three loan categories based on the stage of business development: Shishu (up to ₹50,000) for start-ups, Kishore (₹50,001 to ₹5 lakhs) for growing businesses, and Tarun (₹5 lakhs to ₹10 lakhs) for well-established enterprises. These categories ensure that businesses can get the financial support they need at different stages.

3. Who is eligible for Pradhan Mantri Mudra Yojana?

The eligibility for Pradhan Mantri Mudra Yojana includes individuals, small businesses, proprietary concerns, partnership firms, and more. Businesses in the non-farm sector, such as manufacturing, trading, and services, can apply. The applicant should not have any defaults on previous loans and must have a satisfactory credit history.

4. How can I apply for a Mudra loan?

Entrepreneurs can apply for a Mudra loan through Member Lending Institutions like banks, NBFCs, and MFIs, or via the Udyamimitra portal. Applicants must submit documents such as proof of identity, business registration, and financial records (for larger loans). The process is simple, and loans can be tracked online.

5. What benefits does the Mudra Yojana offer small businesses?

The Pradhan Mantri Mudra Yojana offers several benefits, including collateral-free loans, flexible eligibility criteria, and affordable interest rates. The scheme is designed to reduce the financial burden on small businesses, enabling them to expand, innovate, and contribute to economic growth without the constraints of traditional financing options.

DISCLAIMER:

This blog is provided by the deAsra Foundation (“deAsra”) for informational purposes only, offering insights that may be beneficial for micro, small, and medium-sized enterprises (MSMEs).

PLEASE NOTE: This blog is neither written nor endorsed by any governmental organization nor has any affiliation or connection with any government ministry in India. deAsra makes no warranty or representation regarding the information provided through this blog and disclaims its liabilities in respect thereof, including any liability for authenticity, errors, omissions, or inaccuracies in this blog, if any. Any action on the blog readers’ part based on the information provided in this blog is at his/her/its own risk and responsibility. deAsra reserves the right to modify the information contained in this blog at any time at its sole discretion. deAsra agrees that though all efforts have been made to ensure the veracity of the information in this blog, the same should not be construed as an accurate replacement for authorized commentary on the subject matter before it is used for any legal, financial, or business purposes. deAsra accepts no responsibility for the information’s accuracy, completeness, usefulness or otherwise. In no event will deAsra be liable for any loss, damage, liability, or expense incurred or suffered that is claimed to have resulted from the use or misuse of the information in this blog. We advise you to corroborate the information through authenticated sources and professional consultants before relying on the information stated in this blog. All the information in this blog is for educational and reference purposes only, and we do not make or charge any money to provide this information. Links to the relevant websites included in this blog are provided for readers’ convenience only. deAsra is not responsible for the contents or reliability of linked websites and does not necessarily endorse the views expressed therein. deAsra does not always guarantee the availability of such linked pages. If any content has been unintentionally published or copyrighted material in violation of the law, please don’t hesitate to contact us, and we will have it removed immediately.