The Longer Line: What Data Reveals About India’s Artisan Economy

I recently met someone who works with artisan collectives. Their argument was simple and hard to dismiss: there are too many artisan livelihoods at stake to assume that things will sort themselves out. Markets for artisanal products can be built, they said — through better design, better platforms, better branding. What artisans need is market access; once we solve this problem, things are bound to look up.

I found myself nodding along, and then not. Not because the impulse is wrong, but because I kept wondering what one can see through the enterprise survey data on artisan activities across two rounds of national surveys. The numbers told a more complicated story than any single intervention could address.

How many artisan enterprises are there?

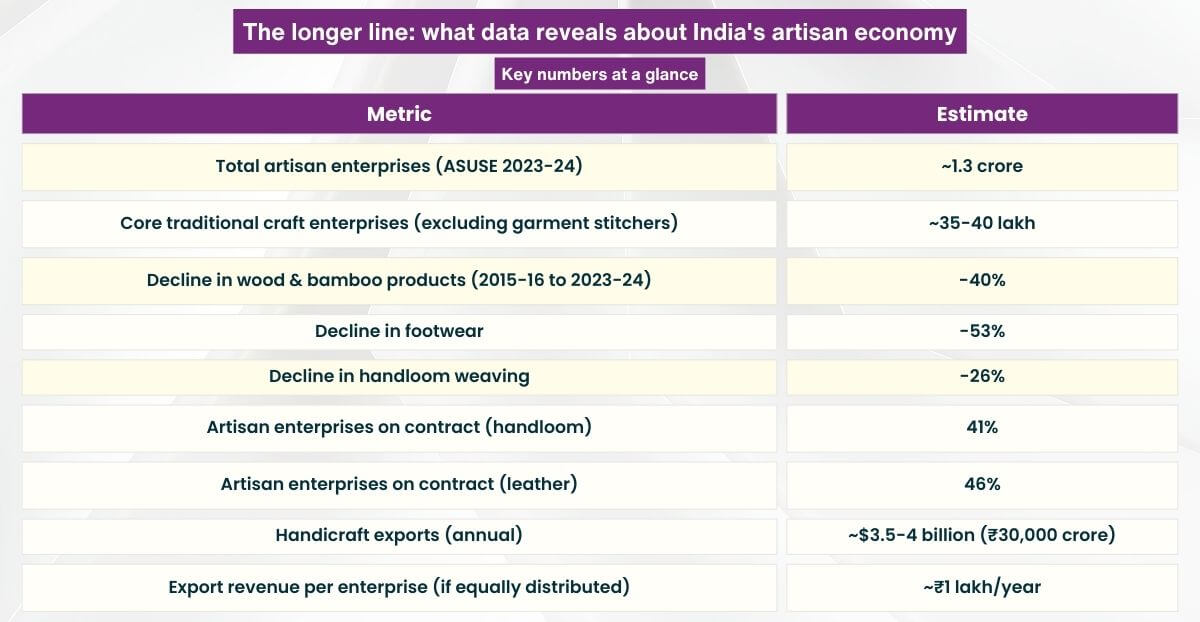

The most recent Annual Survey of Unincorporated Sector Enterprises (ASUSE 2023-24) allows us to count own-account enterprises — single-worker units without hired labour — across industrial classification codes associated with traditional crafts. Using NIC 2008 three-digit codes that capture handloom weaving, textiles, wood and bamboo products, leather, footwear, pottery, metalwork, jewellery, and furniture, we find roughly 1.3 crore such artisan enterprises across the country.

But this headline number is misleading. Nearly 85 lakh of these — about two-thirds — fall under a single category: NIC 141, wearing apparel, which is predominantly women stitching garments at home. Their median annual turnover is ₹67,200, which is about ₹5,600 per month. In rural areas, where 53 lakh of these enterprises are located, 83% are run by women. It is possible that a large part of this is not artisanship in any meaningful sense of the word. It is low-value home-based garment work, and its rapid growth — from 51 lakh in 2015-16 to 85 lakh in 2023-24 — can be better understood as the piece-rate homework providing another livelihood alternative to women working under socio-economic constraints than as a revival of any craft.

Exclude the garment stitchers, and the core traditional craft categories — handloom, carpets and embroidery, wood and bamboo, leather, footwear, pottery, metalwork, jewellery, furniture, and miscellaneous crafts — account for roughly 35-40 lakh own-account enterprises. Even this is an upper bound: industrial classification codes capture the activity, not the craft identity, so a small sawmill operator and a traditional carpenter both fall under NIC 162.

Another way to get these numbers is to look at the numbers under the PM Vishwakarma scheme. As of 3rd March 2025, there are about 2.73 crores applications submitted, while about 30 lakh applicants have completed stage 3 verification and are registered. The total number of applications under PM Vishwakarma are more than double the estimated number of artisanal enterprises through ASUSE 23-24 — a gap that likely reflects a combination of broader trade definitions in the scheme, aspirational registration by those adjacent to artisan work, and the sheer pull of a programme offering toolkits and credit. In this article, we will work with the lower end of these estimates, that there are about 1 crore self-employed artisans in India as of date.

The shrinking core

Comparing the NSS 73rd Round (2015-16) with ASUSE 2023-24 reveals a consistent pattern of decline across every traditional craft category. Wood and bamboo products fell from 10.3 lakh to 6.2 lakh enterprises, a decline of 40%. Footwear fell by 53%. Handloom weaving — perhaps the most culturally iconic artisan activity — fell from 8.9 lakh to 6.6 lakh, a decline of 26%. Jewellery, metalwork, pottery, and furniture each lost between 15% and 19%.

This is not a data blip or a recent phenomenon. It is a structural decline, occurring across categories, in both rural and urban areas. Rural artisan enterprises fell from 35 lakh to 31 lakh; urban from 20 lakh to 17 lakh. The decline is marginally steeper in rural areas, perhaps driven by exposure to incoming substitutes, which is newer and hence more disruptive.

One apparent exception needs noting. NIC 329 — a residual category covering “other manufacturing” including toys, idols, and brooms — appears to have doubled from 3.4 lakh to 6.8 lakh. But a closer look at the five-digit codes reveals that most of the growth is in NIC 32904, the manufacture of articles of personal use such as combs, hair clips, and lighters. This is petty manufacturing of plastic and metal accessories, not traditional craft. The genuine artisanal component of this category — broom-making, idol-carving, toy-making — grew only modestly.

The longer line

What is driving this decline? We do not have a causal explanation from enterprise surveys in the last decade. But the decline of artisanal activities has featured in discussions for a long. We can draw some parallels from there.

The decline of Indian artisans under colonial rule is a well-established fact. A nuanced take on it is that the artisans who survived the arrival of industrial substitutes did so not through state protection but by specialising in non-utilitarian demand — goods purchased for reasons of status, ritual, display, or customisation. The artisans making utilitarian goods — cloth for daily wear, vessels for cooking, implements for farming — were displaced whenever a cheaper, more convenient substitute became available, a ‘Naya Daur’-like story. In a nutshell, the argument is that it is restructuring within a broad decline: factory production grew much faster, but some artisanal activities could remain stable rather than disappearing, precisely because some artisans found non-utilitarian niches.

The same explanation can be applied today, driven not by imperial trade policies but by domestic connectivity along with the availability of substitutes through domestic and import channels. India’s growing investment in roads and more recent surge in logistics chains and e-commerce have eased the arrival of factory-made products into the same village markets where the potter, carpenter, weaver, and cobbler once served a captive consumer base. The substitute does not need to be better — it needs to be cheaper and available.

Consumer preferences have also changed. My grandmother used to clean the grains and groundnuts brought from the kirana shop, using a bamboo product, which she used to buy from members of a community known to make these products (Burud, as they are called in Maharashtra). Now, grains and groundnuts, bought from D-Mart or Blinkit, need not be cleaned before use. My mother switched to D-Mart when she realised this. The loss of demand for a bamboo product is driven by a continuous search for easing the boring or painstaking things in life.

Think of it as drawing a longer line. The artisan’s line — her product, her skill, her market position — has not been erased. But a longer line has been drawn next to it, and the consumer has made her choice. The plastic product from a factory costs less than a brass or bamboo one from an artisan; a newer large enterprise reduces the demand for an artisanal product, as readymade clothes did for tailors. The data confirms this interpretation: the categories declining fastest are precisely the utilitarian ones where industrial substitutes are most readily available — wood products, pottery, basic metalwork, and footwear.

This is not new territory for Indian economic policy. During the early days of planning, the cottage industry was assigned the role of producing consumption goods while heavy industry received the bulk of investment. It was also envisioned that the village and small-scale industries would act as a vehicle for rural employment. Both approaches failed — not because the artisans lacked skill, but because these were ambitions without resources and because the structural forces of industrial substitution were never seriously reckoned with. The pattern of well-intentioned but structurally mismatched policy runs deep, and it has left consequences not only for artisans it tried to protect and grow but for existing and potential firms it constrained in return.

The export arithmetic

One frequently cited response to artisan decline is the potential of export markets. India’s handicraft exports are roughly $3.5-4 billion (₹30,000 crore), and handmade carpets alone account for about 40% of this value. The United States is the single largest destination, absorbing nearly 39% of total handicraft exports.

These are not small numbers. But set them against the artisan population and the arithmetic becomes sobering. Divide ₹30,000 crore across even 30 lakh core artisan enterprises, and you get roughly ₹1 lakh per enterprise per year — if the entire export revenue were distributed equally, which of course it is not. A large share of export value is concentrated among a relatively small number of organised producers and exporters, not dispersed among millions of own-account artisans. The export channel is real and valuable for the artisans connected to it. But it cannot be an income-transformation strategy for the population as a whole. Even a doubling of handicraft exports would not fundamentally alter the livelihood arithmetic for most artisan households.

Not all artisans are entrepreneurs

There is a further complication. A significant fraction of what the surveys classify as “artisan enterprises” are actually dependent workers in putting-out arrangements. In handloom weaving, 41% of own-account enterprises report being on contract. In other textiles — carpets, embroidery, rope-making — the figure is 56%. In leather, it is 46%. These workers receive raw materials from a contractor or master artisan and supply finished goods back at a pre-determined rate. They have no independent market access, no pricing power, and no ability to capture the value of “better marketing.”

Research on subcontracting in India’s informal manufacturing sector has shown that 75-81% of subcontracted household enterprises operate in what is essentially a putting-out relationship, where the parent enterprise controls raw materials, design, and the sale of the final product. Enterprises that are home-based, poorly endowed in assets, and female-headed are more likely to be in such arrangements. For these workers, the relevant policy instrument is not enterprise support but a safety net — formalisation of business transactions, occupational safety, and social security coverage. Calling them “entrepreneurs” and offering them enterprise loans misidentifies the problem. It is not that loans will not help them, but that they will not help the imagined enterprise.

Living with the longer line

None of this is a counsel of despair. It is, however, a counsel against self-deception. The decline of utilitarian artisan production is part of a broader process of creative destruction that has been underway for two centuries and is now accelerated by domestic connectivity and industrial deepening, and imports. There is no point lamenting this decline — the consumer who switches from an artisanal product to a factory-made product is making a rational choice, and no amount of policy can or should reverse it, beyond some demonstrative effect with great expenses. The question we must think about is how to respond honestly.

An honest policy framework would operate at three levels simultaneously.

First, for the export-linked and high-value segment — perhaps 2-5 lakh enterprises in fine carpets, high-end textiles, jewellery, decorative metalwork, and specialised crafts — there is genuine scope for demand expansion. These are the artisans serving non-utilitarian demand, where the buyer values authenticity, craftsmanship, and cultural resonance. Policy here should focus on market-building: connecting artisans to export channels, supporting design innovation (institutions like NID and IITs could take up specific product-improvement challenges), enabling e-commerce presence, and leveraging Geographical Indication tags. On the demand side, influencer-driven awareness campaigns, adoption of artisanal products among younger consumers, and framing artisanal goods as green enterprises could all help. A rewards or points-based scheme that effectively subsidises consumer purchases of certified artisanal products — treating handmade goods the way we treat green energy — is worth considering. These are sensible measures. But they must be understood as serving a relatively small segment of the total artisan population, not as a solution at scale.

Again, we do not have to pick the winners. We should work on easing the access conditions in general, and then individual ingenuity and initiative determine who out of 1 crore falls into this category. It means access to credit on reasonable terms — our data shows that 88-94% of artisan enterprises are credit-distant, structurally separated from formal finance. The PM Vishwakarma scheme, which targets 18 specific artisan trades with skilling, toolkits, and credit support, is a step in this direction. But the honest measure of success for such programmes is not whether they turn potters into exporters, but whether they provide a floor of dignity and security while the structural transition runs its course.

Second, for the broad middle — the bulk of 30+ lakh core artisan own-account enterprises making utilitarian or semi-utilitarian goods — the realistic policy target is livelihood stabilisation, not income transformation. This means robust social protection: health insurance, pensions, housing support – and not any specific enterprise or industrial policy aimed at artisans.

Third, and perhaps most importantly, the transition away from artisanship that is already underway must be made less painful and not opposed explicitly. The data shows 12 lakh fewer core artisan own-account enterprises in eight years. People are leaving. In many artisan households, this choice is already being made inter-generationally: the parents weave, the children study and move away from parental occupation with or without acquisition of parental skills. This exit needs policy support, not policy resistance. Skilling programmes should build on existing manual dexterity — a weaver’s hand-eye coordination, a metalworker’s understanding of materials, and a carpenter’s spatial reasoning — to prepare artisans or their children for occupations where these skills command higher productivity. The draft skill policy 2025 has recognised this occupational skilling aspect, and that is the right recognition.

Equally important is the systematic documentation of artisanal processes and techniques — not as a museum exercise, but as a knowledge base that might find unexpected applications elsewhere. The mapping of artisan skills to industrial sectors where manual precision and material knowledge are valued could accelerate a transition that is already happening organically through market forces. But policy should not aim at making the matching happen. Networks and markets are great conduits of information. A broad policy of unconditional income support, which respects as well as highlights the individual choice, can achieve lots of things that explicit sectoral policies aim to achieve.

The person I met who works with artisan collectives is not wrong that the numbers are too large to ignore. Where I find myself departing is in the diagnosis and the prescription. The problem facing most artisans is not poor marketing or insufficient enterprise support. The problem is the longer line — the factory substitute that reaches the village market via the very roads and logistics networks that represent India’s development success. The artisan’s product has not become worse. The consumer’s alternatives have become better and cheaper, and consumer preferences have evolved irreversibly in the direction of ease and efficiency.

Thinking that better market access or design interventions will solve this problem for 30-40 lakh artisan enterprises is, I believe, not well supported by the evidence. It will work for some thousands, perhaps even a few lakhs, at the high end. For the rest, the honest objectives are livelihood security, dignified transition, and the recognition that creative destruction, while painful for those in its path, is not a failure of policy. It is the process by which economies grow. The task of policy is not to stop the process, but to ensure that those displaced by it are not left behind. And while markets create and destruct the longer and shorter lines, and government responds through politics and policy, the society must not forget – the art and craft should not be lost, though we must not lament when livelihoods depending on them are fading away.

Explore More Insights

Interested in more research and analysis on entrepreneurship, livelihoods, and India’s evolving economy? Discover our latest blogs and data-driven perspectives.