Simplified Guide to Filing Income Tax Returns for Proprietors in India

Introduction

Income Tax Return (ITR) filing is vital for business owners, especially those operating as sole proprietors or in a proprietorship firm. Let’s explore the basics of ITR for proprietors and ITR for proprietorship firms, and underscore the importance of compliance, with a specific focus on GST in India.

Understanding the Basics

Income Tax Return for Proprietorship:

An Income Tax Return (ITR) for a sole proprietor or proprietorship firm is like a financial report card. It’s a document where business owners disclose their earnings, expenses, and other financial details to the tax authorities. By doing this, they let the government know how much tax they should pay.

Differences between Individuals and Proprietorship Firms:

Structure:

- Individuals: When you’re an individual, your ITR covers your income, which could include your salary, rent you earn, and any other sources of personal income.

- Proprietorship Firms: Proprietors file an ITR for their business income. In a proprietorship, there’s no legal separation between the business and its owner.

Tax Rates:

- Individuals: Individual tax rates vary based on how much you earn.

- Proprietorship Firms: Proprietorship firms are subject to distinct business tax rates that may differ from individual tax rates.

Deductions and Exemptions:

- Individuals: Individuals can claim deductions and exemptions to reduce the income they pay tax on.

- Proprietorship Firms: Proprietors can also avail of business-related deductions to lower their taxable income.

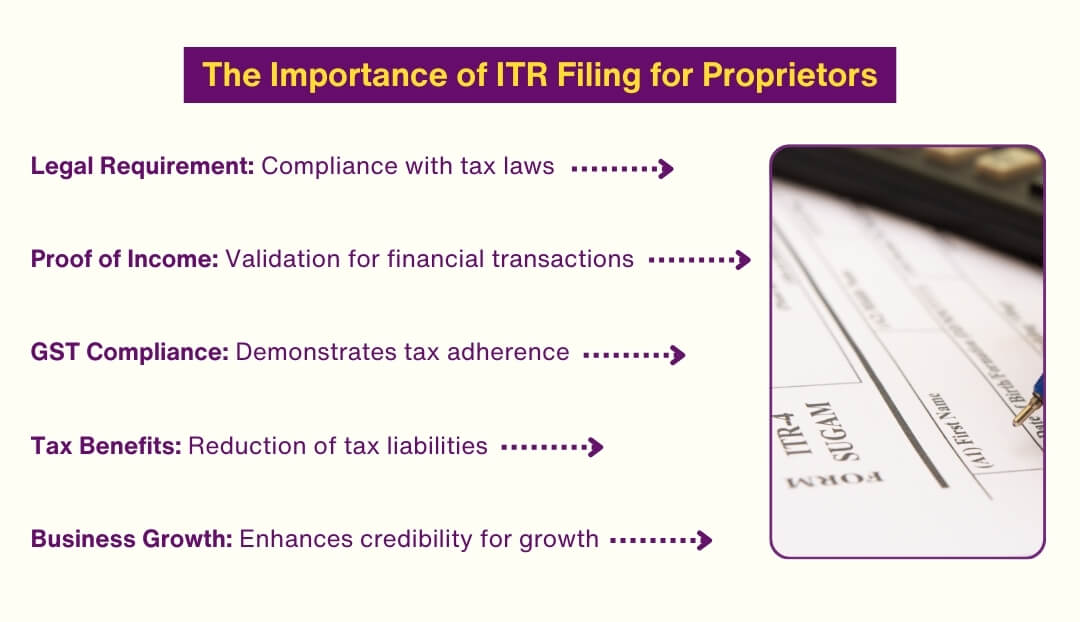

Importance of ITR for Proprietors:

Now, let’s dive into why ITR filing is so crucial for proprietors:

- Legal Requirement:

It’s the law! Sole proprietors and proprietorship firms must file their ITR to comply with tax regulations. Not doing so can lead to certain fines and legal troubles.

- Proof of Income:

The ITR acts as proof of your income. It can be crucial when applying for loans, visas, or government contracts.

- GST Compliance:

In the Indian context, particularly concerning GST, filing an ITR demonstrates your commitment to following tax rules. This helps maintain your business’s reputation and prevents tax evasion allegations.

- Tax Benefits:

Filing ITR allows proprietors to claim deductions, tax credits, and exemptions, which can significantly reduce the tax they need to pay, saving them money.

- Business Growth:

Maintaining ITR records can also boost your chances of securing investments, forming partnerships, and growing your proprietorship business.

Types of Income for Proprietors

When filing Income Tax Returns (ITR) as a proprietor or for a proprietorship firm, it’s essential to understand the various types of income that need to be reported. Here, we’ll break down these income sources and discuss how GST (Goods and Services Tax) in India is integrated with ITR for proprietors.

- Income from Business:

As a proprietor, the primary income source is your business operations. This includes the money you earn from selling goods or providing services. It’s crucial to keep accurate records of your business income.

- Income from Other Sources:

Apart from your business income, you might have income from other sources, such as interest on savings accounts, rental income from property, or capital gains from investments. These sources should also be reported in your ITR.

- Income Tax Slabs and Rates for Proprietors:

The income tax rates and slabs for proprietors differ from those for salaried individuals. Proprietors are subject to specific tax rates based on their income. These rates can change yearly, so staying updated with the latest tax brackets is essential.

GST and ITR for Proprietors

Integration of GST with ITR:

GST is integrated with your ITR as it impacts your taxable income. Here’s how it works:

Reporting GST-related income and expenses:

- When filing your ITR, you must report your GST-related income. This includes the total value of sales and services provided on which GST was collected.

- On the expenses side, you can claim an input tax credit for the GST you’ve paid on goods and services used for your business. This helps reduce your taxable income.

- Ensure accurate reporting of your GST figures to avoid discrepancies between your ITR and GST returns.

Preparing for ITR Filing:

Filing your Income Tax Return (ITR) is a necessary part of being a business owner in India. Whether you’re a sole proprietor or operate a proprietorship firm, the process requires gathering specific documents and calculating your income and tax liability. Let’s go through the essential steps to prepare for ITR filing, focusing on GST in India.

Gathering Necessary Documents:

- Business Income Records:

Your business income records are the backbone of your ITR filing. These records include invoices, receipts, and financial statements that show your business earnings. Ensure these documents are accurate and up-to-date. - GST Returns and Records:

In India, having your GST returns and related records ready is crucial. These documents will help you report your income and expenses accurately. - Other Income Documents:

In addition to your business income, you may have other sources of income, such as investments or rental income. Gather relevant documents, such as rent agreements or bank statements, to account for all your income.

Calculating Total Income and Tax Liability

Once you’ve collected the necessary documents, it’s time to calculate your total income and tax liability:

- Business Income:

Sum up all your business income from the records you’ve gathered. This includes sales, service income, and other money earned through business activities. - Other Income:

Remember to add any other income sources you’ve identified from your documents, such as rental income or investment gains. - Deductions and Expenses:

Deduct any eligible business expenses, deductions, and exemptions allowed under the tax laws to reduce your taxable income. - Tax Liability:

Calculate your tax liability based on your total income, deductions, and the applicable tax rates for proprietors. You can choose online tax calculators or seek professional assistance to ensure accuracy.

Filing the ITR

Filing your Income Tax Return (ITR) is a crucial responsibility for proprietors and proprietorship firms in India. It’s a process that involves choosing the correct ITR form, accurately filling it out, and meeting deadlines. Let’s go through the steps involved in ITR filing, focusing on GST in India.

Choosing the Appropriate ITR Form

- Selecting the correct ITR form is vital. For proprietors, ITR-3 is usually the applicable form. Ensure you choose the form that matches your income sources and business structure.

Filling Out the ITR Form

- Personal and Business Information: Start by providing your personal and business details as required in the form.

- Income Details: Report your total income, including business income and other sources like rent or investments.

- Deductions and Exemptions: List all eligible deductions and exemptions to reduce your taxable income. Ensure accurate reporting.

E-filing and Offline Filing Options

- E-filing: E-filing is a convenient and preferred method for ITR filing. You can do it online through the Income Tax Department’s official website.

- Offline Filing: If you choose to file offline, make sure to download the relevant ITR form, fill it out, and submit it physically to the tax office.

Deadline for ITR Filing

- Stay Informed: Be aware of the ITR filing deadlines, which can vary yearly. Failing to file on time may result in penalties.

Deductions and Tax-saving Tips

Eligible Deductions for Proprietors

- Claim Business Expenses: Ensure you claim all legitimate business expenses to reduce your taxable income.

- Section 80 Deductions: Explore Section 80C, 80D, and other provisions for deductions related to investments, insurance, and healthcare.

Tips for Minimizing Tax Liability

- Tax Planning: Plan your finances strategically to minimize your tax liability. Seek advice from financial experts if needed.

Common Challenges and Solutions

Addressing Common Mistakes

- Double-check: Review your ITR form carefully to avoid common mistakes, such as incorrect data or missing documents.

Handling Discrepancies and Notices

- Respond Promptly: If you receive a notice or find discrepancies, address them promptly to avoid legal issues.

Seeking Professional Assistance

- Tax Consultants: Consider hiring tax consultants or professionals to ensure accurate ITR filing and compliance with GST regulations.

ITR Filing Made Easy with deAsra

Filing Income Tax Returns (ITR) can feel overwhelming for new and experienced business owners. That’s where deAsra comes in. We offer a service to simplify ITR filing for businesses of all types. We aim to help you follow the tax rules without the hassle, ensuring your business keeps running smoothly.

At deAsra, we understand every business has its own needs. Our friendly team offers personalized support designed just for you. Whether you need help figuring out how to file your ITR, gather the proper documents, or understand what to do after filing, we’re here. Here’s what we offer:

- A chat to understand your business and what you need for your ITR.

- Support in collecting all the documents you need to file your ITR.

- Help with filling out and submitting your ITR forms.

- Advice on how to manage your taxes after you’ve filed your ITR.

Choosing deAsra for your ITR filing means getting our full support and knowledge. We’re all about helping small businesses and entrepreneurs. With us, ITR filing becomes something you don’t have to worry about, so you can focus more on growing your business.

Want more information on how we can help with ITR filing or have other questions? Visit here , or reach out to deAsra today. We’re excited to help your business progress and stay on top of tax filing.

Conclusion

Filing your ITR as a proprietor or proprietorship firm in India can be complex, but it’s essential for legal compliance and financial stability. You can navigate the process effectively by choosing the correct ITR form, accurately reporting your income and deductions, and meeting deadlines. Remember to stay informed about the changes in tax laws and pursue professional assistance when needed to ensure a hassle-free and compliant ITR filing experience.

FAQs

1. What is the deadline for filing an ITR for proprietors?

The deadline for filing ITR for proprietors typically falls on July 31st of each assessment year. However, it’s advisable to check the specific deadline for the current financial year, as it can change.

2. How do I report GST-related income in my ITR?

You should report your GST-related income in the relevant sections of your ITR form. Include the total value of sales and services on which GST was collected.

3. Can I claim deductions for business expenses in ITR?

Yes, you can claim deductions for fair business expenses in your ITR. Ensure you maintain proper records and report them accurately to reduce your taxable income.

4. What should I do if I receive a notice from the Income Tax Department?

If you receive a notice, don’t panic. Review the notice carefully, understand the issue, and respond promptly with the requested information or clarifications.

5. Is it necessary to hire a CA or tax professional for ITR filing?

While it’s not mandatory, hiring a CA or tax professional can ensure accurate and hassle-free ITR filing, especially if you have complex financial situations.

6. What are the consequences of not filing ITR as a proprietor?

Not filing ITR can result in penalties and legal troubles. It may also affect your ability to obtain loans, visas, or government contracts.

7. Can I file ITR online if I have multiple businesses as a proprietor?

Yes, you can file an ITR online even if you have multiple businesses. Ensure you choose the appropriate ITR form and report income from each business separately.

8. How can I check the status of my filed ITR?

One can check the status of their filed ITR on the official Income Tax Department website using your Permanent Account Number (PAN) and acknowledgement number.

9. Are there any penalties for late ITR filings for proprietors?

Yes, there are penalties for late ITR filings. Depending on the delay, you may be liable for penalties, and interest.

10. Can I revise my ITR if I made a mistake in the initial filing?

Yes, you can revise your ITR if you made a mistake in the initial filing. Use the online portal to submit a revised return, but make sure to do it within the specified timeframe.

Disclaimer:

This blog is provided by the deAsra Foundation (“deAsra”) for informational purposes only, offering insights that may be beneficial for micro, small, and medium-sized enterprises (MSMEs).

PLEASE NOTE: This blog is neither written nor endorsed by any governmental organization nor has any affiliation or connection with any government ministry in India. deAsra makes no warranty or representation regarding the information provided through this blog and disclaims its liabilities in respect thereof, including any liability for authenticity, errors, omissions, or inaccuracies in this blog, if any. Any action on the blog readers’ part based on the information provided in this blog is at his/her/its own risk and responsibility. deAsra reserves the right to modify the information contained in this blog at any time at its sole discretion. deAsra agrees that though all efforts have been made to ensure the veracity of the information in this blog, the same should not be construed as an accurate replacement for authorized commentary on the subject matter before it is used for any legal, financial, or business purposes. deAsra accepts no responsibility for the information’s accuracy, completeness, usefulness or otherwise. In no event will deAsra be liable for any loss, damage, liability, or expense incurred or suffered that is claimed to have resulted from the use or misuse of the information in this blog. We advise you to corroborate the information through authenticated sources and professional consultants before relying on the information stated in this blog. All the information in this blog is for educational and reference purposes only, and we do not make or charge any money to provide this information. Links to the relevant websites included in this blog are provided for readers’ convenience only. deAsra is not responsible for the contents or reliability of linked websites and does not necessarily endorse the views expressed therein. deAsra does not always guarantee the availability of such linked pages. If any content has been unintentionally published or copyrighted material in violation of the law, please don’t hesitate to contact us, and we will have it removed immediately.