Financing Your Franchise Business: Exploring Your Loan and Funding Options

Venturing into a franchise business demands strategic financial planning from the outset, as securing funds can unlock doors to established brands with proven models. Entrepreneurs often overlook the nuances of funding, yet mastering this aspect transforms aspirations into thriving ventures. In the dynamic landscape of franchise business in India, where sectors like food, education, and retail flourish, understanding loan options ensures sustainable growth. For a deeper dive into the advantages and drawbacks, explore this insightful blog on the pros and cons of owning a franchise business, which highlights how brand recognition can bolster your funding journey while cautioning against hidden costs.

Bold keywords like best franchise business choices emphasise the need for alignment with personal strengths and market demand. Whether eyeing a franchise business in wellness or quick-service restaurants, initial capital requirements vary, but smart financing bridges the gap. This guide draws on expert insights from the deAsra and dreamBIG podcast, where Mr. Aniket More shares practical wisdom on scaling without overextending resources.

Understanding the Basics of Franchise Funding

Launching a franchise business involves more than selecting the best franchise business; it requires a clear grasp of funding essentials. Many aspiring owners face hurdles in accessing capital, yet options abound from traditional loans to innovative schemes. In the franchise business in India, banks assess personal profiles alongside business viability, often prioritising credit scores and promoter contributions. Preparing documentation meticulously can turn potential rejections into approvals, setting the stage for long-term success.

Franchise funding differs from starting an independent venture due to the built-in support of established systems. However, investors must demonstrate local demand and realistic projections to lenders.

Common Challenges in Securing Franchise Loans

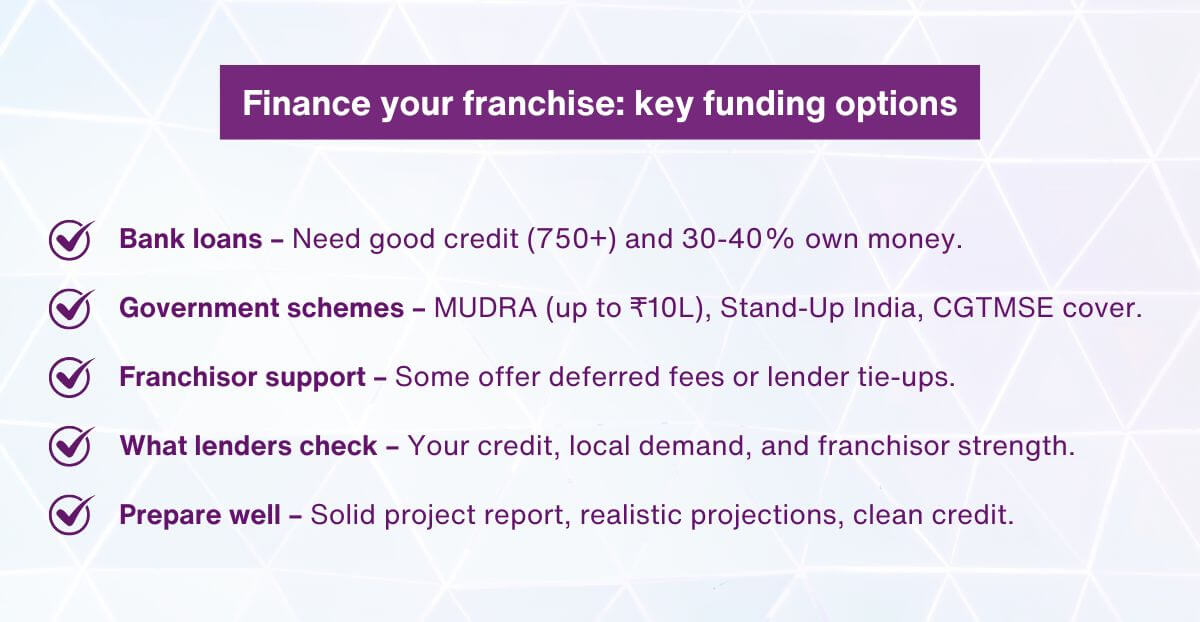

Securing loans for a franchise business frequently encounters obstacles unrelated to the brand’s strength. Issues like weak credit profiles or inadequate project reports lead to denials, even for the best franchise business opportunities. In the franchise business in India, banks scrutinise personal finances, demanding scores above 750 for favourable terms. Addressing these early—by settling debts and optimising credit utilisation—enhances approval chances significantly.

Overreliance on brand reputation without local feasibility data is another pitfall. Lenders seek evidence of sustainable cash flows, such as rent-to-revenue ratios under 10%. Mr. Aniket More notes in the deAsra and dreamBIG podcast, “With franchising, the sky’s the limit. You can expand within your state, across India, or even internationally.” This underscores the importance of robust planning to overcome fears and secure funding.

Traditional Bank Loans and Their Requirements

Traditional bank loans remain a cornerstone for funding a franchise business, offering structured terms for those with solid profiles. In the franchise business in India, MSME term loans and SME working capital options provide essential capital, often backed by schemes like CGTMSE for collateral-free access up to ₹10 crore. Banks evaluate creditworthiness, experience, and business plans rigorously, preferring applicants with at least 30-40% personal investment.

Preparation involves crafting detailed project reports with conservative revenue forecasts and break-even timelines of 12-18 months. For the best franchise business in sectors like retail or education, aligning with bank preferences—such as proven footfall—boosts success.

Government Schemes Supporting Franchise Expansion

Government initiatives play a pivotal role in financing franchise businesses in India, making opportunities accessible to diverse entrepreneurs. Schemes like MUDRA under PMMY offer loans up to ₹10 lakh with minimal documentation, ideal for micro-level franchise business entries. Stand-Up India targets women and SC/ST groups with funding from ₹10 lakh to ₹1 crore, fostering inclusive growth in the best franchise business arenas.

PMEGP provides subsidy-based loans for new units, including franchises, emphasising manufacturing and services. These programmes, combined with CGTMSE coverage, reduce risks for lenders and borrowers alike.

Franchisor Financing and Innovative Options

Franchisors often extend financing to attract partners, easing entry into a franchise business. This includes deferred fees or partnerships with lenders, reducing upfront burdens. In the best franchise business setups, like FOFO models, franchisors provide benchmarks and training certifications to strengthen loan applications. deAsra supports and engages by connecting entrepreneurs to resources, including the Franchise for Business Growth page, which details models and checklists.

Globally inspired options like Rollovers for Business Startups (ROBS) allow using retirement funds tax-free, though less common in India. SBA loans, akin to US small business administration support, find parallels in MSME schemes here. Mr. Aniket More advises, “To succeed, you need to shift your focus. Instead of growing your business, focus on the franchisee’s growth.” This mindset aids in negotiating favourable franchisor terms.

Overcoming Rejection and Building a Strong Application

Loan rejections in the franchise business in India stem from fixable issues like poor documentation or high debt levels. Reviewing feedback post-denial—improving credit scores or increasing contributions—turns setbacks into opportunities. For the best franchise business, persistence with refined projections pays off, as many succeed after initial hurdles.

International Perspectives: SBA Loans and ROBS

While India-focused, insights from SBA loans highlight guaranteed funding for small ventures, adaptable through local equivalents like CGTMSE. These cover up to 85% of defaults, encouraging banks to lend to franchise business starters. In the franchise business in India, blending such mechanisms with sector-specific strategies yields the best franchise business outcomes.

ROBS enables tapping retirement savings without penalties, funding setups penalty-free. Though regulatory differences exist, similar tax-efficient options emerge via provident funds. These tools, when used judiciously, complement traditional paths for ambitious entrepreneurs.

Conclusion

Financing a franchise business blends preparation, diverse options, and expert guidance to achieve growth. From government schemes to franchisor support, avenues exist for every profile in the franchise business in India. Embracing systematic planning and resources from deAsra ensures the best franchise business ventures thrive, turning financial challenges into stepping stones for success.

FAQs

1. What are the key documents needed for a franchise loan application?

Essential documents include a detailed project report, proof of promoter contribution, credit score reports, and local market analysis. Banks in the franchise business in India also require franchise agreements and financial projections showing realistic break-even points. Preparing these with deAsra’s checklists streamlines the process, boosting approval rates for your chosen best franchise business.

2. How does CGTMSE benefit franchise investors?

CGTMSE offers collateral-free loan coverage up to ₹10 crore, reducing barriers for starting a franchise business. It guarantees 75-85% of defaults, encouraging banks to lend to viable proposals. In the franchise business in India, this scheme supports nano-entrepreneurs in sectors like retail, making the best franchise business more accessible without heavy assets.

3. Is experience mandatory for securing franchise funding?

While not always required, relevant experience strengthens applications for a franchise business. Lenders value operational knowledge, but franchisor training can compensate. In the franchise business in India, adding a co-promoter with expertise or highlighting transferable skills from sales boosts credibility for the best franchise business opportunities.

4. What rent-to-revenue ratio should I aim for in projections?

Aim for 5-10% in retail or 6-8% in the food sector to demonstrate sustainability in your franchise business. Exceeding these raises red flags for lenders. In the franchise business in India, aligning ratios with local data ensures realistic plans for the best franchise business, as emphasised in deAsra resources.

5. Can home-based businesses qualify for franchise loans?

Yes, home-based models in services or education often qualify for funding in franchise businesses in India. Banks assess viability like any franchise business, focusing on demand and systems. deAsra supports and engages such entrepreneurs, helping tailor applications for the best franchise business fits with lower overheads.