Quarterly Estimated Business Taxes: Who Needs to Pay Them and How to Avoid Penalties

Quarterly estimated business tax payments form a critical part of financial discipline for entrepreneurs across India. Many owners underestimate the impact of timely advance business income tax contributions, only to face unexpected interest charges later. This structured guide outlines the rules, deadlines, and practical steps to ensure compliance while maintaining a healthy cash flow.

Drawing from expert discussions on the deAsra dreamBIG podcast, it shows how systematic processes turn business tax obligations into manageable routines. For more practical resources, visit deAsra’s detailed section on accounting and taxation.

Understanding Quarterly Estimated Business Taxes

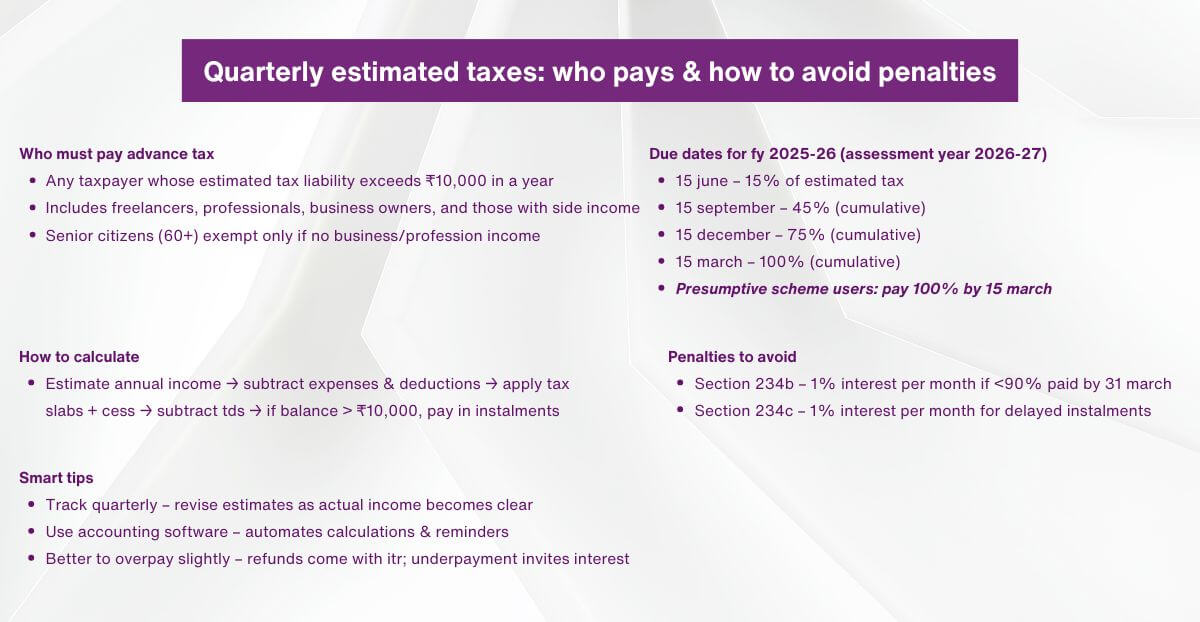

Quarterly estimated business tax, commonly referred to as advance tax, requires taxpayers to pay their income tax liability in four instalments during the financial year. This system, governed by Sections 207–219 of the Income Tax Act, prevents large lump-sum payments at the time of ITR filing. It applies whenever the estimated tax liability for the year exceeds ₹10,000 after adjusting for TDS or TCS.

The mechanism promotes better cash-flow planning. Businesses earn income throughout the year, so spreading tax payments aligns outflows with inflows. For small and mid-sized enterprises, this approach reduces year-end stress and improves financial predictability. Regular estimation also helps owners spot cash-flow gaps early.

Who Needs to Pay Advance Business Taxes

Any individual or entity whose estimated business income tax liability for the financial year crosses ₹10,000 must pay advance tax. This rule covers freelancers, professionals, traders, service providers, and companies. Even salaried people with side income—such as interest, rentals, or freelancing—may need to pay if the total liability exceeds the threshold after TDS.

Senior citizens aged 60 years or older are exempt only if they have no business or professional income. Those who run a business or practice a profession remain liable. NRIs with taxable income in India follow the same rule when the estimated liability surpasses ₹10,000. Presumptive taxation schemes (Sections 44AD, 44ADA, 44AE) offer simplified options, often allowing full payment by the final date.

Due Dates and Instalment Structure for FY 2025-26

For most taxpayers, the schedule is clear: 15% of the estimated liability by 15 June, 45% (cumulative) by 15 September, 75% by 15 December, and 100% by 15 March. These dates apply to FY 2025-26 (Assessment Year 2026-27).

Under presumptive schemes for small businesses and professionals, 100% of business tax is due by 15 March. Goods transport operators opting for Section 44AE follow the regular four-instalment pattern. Marking these dates in a compliance calendar prevents last-minute rushes and keeps payments aligned with actual earnings.

How to Calculate Your Advance Tax Liability

Start by estimating gross income from all sources for the year. Deduct eligible expenses and Chapter VI-A deductions (such as 80C for PPF, LIC, or ELSS, and 80D for health insurance). Apply the appropriate tax regime—old or new—then add surcharge (if income exceeds ₹50 lakh) and 4% health and education cess. Subtract any TDS or TCS already deducted.

If the net business income tax liability is above ₹10,000, divide the amount into four instalments. Review and revise the estimate every quarter as actual income becomes clearer. Online calculators and accounting software make this process faster and more accurate. Consistent tracking avoids underpayment surprises.

Avoiding Penalties and Interest Charges

Paying less than 90% of the total liability by 31 March triggers 1% monthly interest under Section 234B on the shortfall. Delayed instalments attract 1% interest per month under Section 234C for the relevant period—three months for the first three instalments and one month for the March payment. These charges directly reduce profitability.

The best defence is a reliable system. Use compliance calendars, set reminders, and follow standard operating procedures for estimation and payment. Overpayments are refunded during ITR processing, so conservative estimates are safer than risky underpayments. Timely compliance also strengthens credibility with banks and investors.

Using Technology to Simplify Business Tax Payments

Modern accounting software and AI tools automate much of the quarterly estimated business tax process. Bank statements import automatically, GST data pulls from portals, and OCR reads physical bills. These features reduce manual entry errors and save time.

Cloud-based platforms suit businesses with multiple locations, while domain-specific software handles unique needs such as batch tracking or expiry dates. Virtual CFO services provide expert oversight at a fraction of full-time cost. As technology evolves, routine tasks become faster, allowing owners to focus on core operations.

Conclusion

Quarterly estimated business tax is a straightforward obligation when approached systematically. By understanding who must pay, following due dates, calculating accurately, and using technology, entrepreneurs avoid penalties and maintain healthy cash flows. deAsra supports and engages business owners through the dreamBIG podcast and practical resources, helping them build disciplined financial habits. Consistent compliance turns business income tax from a burden into a foundation for sustainable growth.

FAQs

1. Who is exempt from paying quarterly estimated business tax?

Senior citizens aged 60 or above are exempt only if they have no business or professional income. Everyone else with an estimated liability over ₹10,000 after TDS/TCS must pay advance business tax.

2. What happens if I miss one of the instalment dates?

Missing an instalment triggers 1% monthly interest under Section 234C on the shortfall for the relevant period. Paying the remaining amount in the next instalment limits further charges, but early correction is always better.

3. Can I pay the full amount in March under presumptive taxation?

Yes, small businesses and professionals under Sections 44AD or 44ADA can pay 100% of their business income tax by 15 March. Goods transport operators under 44AE must follow the four-instalment schedule.

4. How do I correct a mistake made in an advance tax challan?

Log in to the e-filing portal, go to Services → Challan Correction, select the correction type (assessment year, major head, or minor head), enter details, and verify using OTP, DSC, or EVC. Keep the transaction ID to track progress.

5. Is advance tax required even if TDS covers most of my liability?

Yes, if the remaining liability after TDS exceeds ₹10,000, you must pay advance business tax. Regular review of income sources ensures you catch any shortfall early.