The Credit Guarantee Fund Scheme has been ongoing since 2000, with regular modifications and enhancements over the years to make it more effective and inclusive for Micro and Small Enterprises (MSEs).

Credit Guarantee Fund Scheme: Easy Business Loans Without Collateral

Small businesses in India power the nation’s growth, with over 63 million running shops, factories, and services. But getting money to grow can be hard, especially when banks ask for collateral like land or houses. The credit guarantee fund scheme (CGTMSE) solves this by offering loans without needing significant security.

This blog explains how the credit guarantee fund scheme works, who can use it, and how it helps small businesses get funds easily. It covers loan limits, benefits, and steps to apply, showing how Indian owners can expand with help from this funding support guide. With CGTMSE, your business dreams can come true without risking your home.

What Is the Credit Guarantee Fund Scheme?

The credit guarantee fund scheme is a government plan to help small businesses borrow money without collateral. Started in 2000, it’s run by the credit guarantee fund trust for micro and small enterprises (CGTMSE), set up by the Ministry of Micro, Small and Medium Enterprises and the Small Industries Development Bank of India (SIDBI).

The idea is simple: if a small business can’t repay a loan, the trust promises to cover most of the loss for the bank. This makes banks happy to lend up to ₹2 crore – or even ₹5 crore since 2023 – without asking for big assets. It’s a lifeline for micro and small enterprises (MSEs) across India.

How Does It Work?

The credit guarantee fund scheme acts like a safety net. When you borrow from a bank or lender signed up with the credit guarantee fund trust for micro and small enterprises, they don’t need your house or shop as a backup. Instead, the trust guarantees to pay back 50% to 85% of the loan if you can’t. For loans up to ₹5 lakh, micro businesses get 85% cover. Women-run firms or businesses in the Northeast get 80%. For bigger loans up to ₹2 crore, it’s 50%. This promise makes banks feel safe, so they say yes to small businesses more often.

Who Can Use the Credit Guarantee Fund Scheme?

- Eligible businesses: Both new and existing Micro and Small Enterprises (MSEs) such as shops, factories, or service providers.

- MSME definition:

- Micro enterprises: Investment up to ₹1 crore in equipment and turnover up to ₹5 crore annually.

- Small enterprises: Investment up to ₹10 crore and turnover up to ₹50 crore annually.

- Credit coverage: The scheme covers collateral-free credit facilities up to ₹10 crore for eligible MSEs.

- Type of loans: Only loans extended by banks and financial institutions without collateral are covered.

- Exclusions: Farms, schools, and self-help groups are not eligible.

- Wide lender network: Supported by over 130 lending institutions, including major banks like SBI, HDFC, and ICICI, through the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE).

Loan Limits and Costs

The credit guarantee fund scheme offers loans up to ₹2 crore without collateral. Since April 2023, this limit jumped to ₹5 crore for some cases, giving bigger dreams a chance. You can use the money for machines, stock, or daily costs – whatever your business needs. There’s a small fee: 1.5% of the loan as a one-time guarantee fee, plus 0.75% yearly. For tiny loans up to ₹5 lakh, it’s lower – 1% once and 0.5% yearly. The credit guarantee fund trust for micro and small enterprises keeps these costs affordable so more owners can join in.

Benefits of the Credit Guarantee Fund Scheme

- Collateral-free credit: MSMEs can get loans without risking assets like a home, shop, or machinery.

- Enhanced access to credit: Banks and financial institutions are more willing to lend, as loans are backed by the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE).

- Coverage up to 85%: Depending on the loan amount and category (including women-led and new enterprises), up to 85% of the credit facility is guaranteed.

- Support for new and women-led businesses: Helps entrepreneurs who often face the toughest challenges in securing finance.

- Large-scale impact: In 2023–24, guarantees worth ₹2 lakh crore were approved, proving its role as a game-changer for small businesses.

Read our top government loan schemes blog and grow without stress.

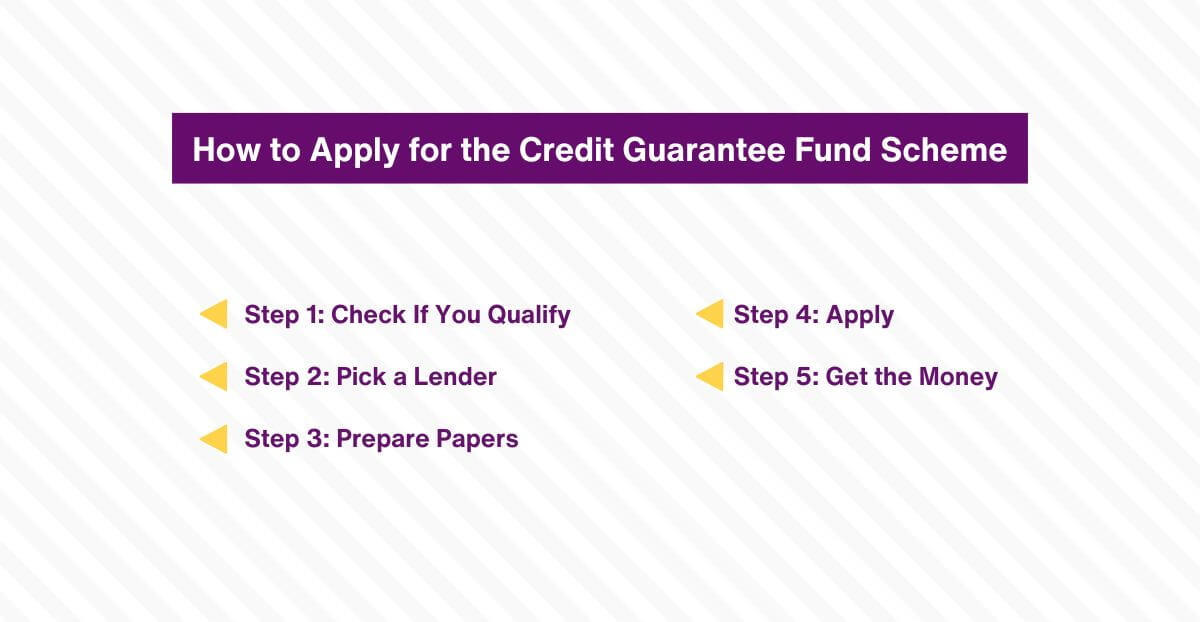

How to Apply for the Credit Guarantee Fund Scheme

Getting a loan under the credit guarantee fund scheme is straightforward. Follow these steps:

- Step 1: Check If You Qualify

Make sure your business fits the MSME size rules. You’ll need proof like a Udyam Registration certificate. - Step 2: Pick a Lender

Visit a bank or lender signed up with the credit guarantee fund trust for micro and small enterprises. Public banks like SBI or private ones like Axis Bank work. - Step 3: Prepare Papers

Bring your ID (Aadhaar, PAN), business address proof, bank statements, and a plan showing how you’ll use the loan. No big collateral is needed! - Step 4: Apply

Fill out the bank’s form. They’ll check your business idea and send it to the credit guarantee fund trust for micro and small enterprises for approval. - Step 5: Get the Money

If approved, the bank gives you the cash. The trust covers the guarantee, so you start growing.

Why It’s Great for India in 2025

Small businesses in India are growing fast – they make up 96% of all factories and produce 40% of the country’s goods. But many can’t get loans because they don’t own big things like houses. The credit guarantee fund scheme helps by giving them money without needing those assets. In 2024, over 900 million people use the internet, and 80% pay with UPI on their phones – everything is going digital.

Tools like Razorpay make payments easy, but businesses still need cash to keep going. The credit guarantee fund trust for micro and small enterprises gives loans without old-style security, fitting this new digital world. By 2025, online shopping will reach ₹12 trillion, and this scheme keeps small businesses ready to grow.

Tips to Make It Work for You

- Plan Your Loan: Know exactly what you need – machines, stock, or rent – and show the bank a clear idea.

- Keep Records: Good bookkeeping impresses lenders and fits your accounting checklist for small businesses.

- Pay on Time: Repaying well builds your credit score for future loans.

- Ask Questions: Talk to your bank about fees or terms to avoid surprises.

Final Thoughts

The credit guarantee fund scheme is a golden chance for India’s small businesses. It cuts the worry of collateral and opens doors to cash for growth. With the credit guarantee fund trust for micro and small enterprises backing you, banks trust your dreams. Whether you’re starting a shop or expanding a factory, this scheme makes loans simple and safe. In 2025, as India’s economy races ahead, use this plan to build your future. Apply today, grow tomorrow – no big risks, just big wins.

FAQs

1. What is the credit guarantee fund scheme?

The credit guarantee fund scheme is a plan to help small businesses in India get loans without giving big assets like a house. Run by the credit guarantee fund trust for micro and small enterprises, it promises banks to cover most of the loan if you can’t pay back, making borrowing easier.

2. Who can apply for the credit guarantee fund scheme?

Small and micro businesses – like shops or factories – can use the credit guarantee fund scheme if they fit MSME rules. You need a yearly income of up to ₹50 crore and equipment worth up to ₹10 crore. Farms or schools can’t apply, but new or old firms can.

3. How much money can I get from the credit guarantee fund scheme?

With the credit guarantee fund scheme, you can borrow up to ₹10 crore since 2023 – without collateral. The credit guarantee fund trust for micro and small enterprises covers 50% to 85% of it, so banks feel safe lending you cash for machines or stock.

4. Do I need to pay fees for the credit guarantee fund scheme?

Yes, the credit guarantee fund scheme has small fees. You pay 1.5% of the loan once and 0.75% yearly – or less for tiny loans up to ₹5 lakh. The credit guarantee fund trust for micro and small enterprises keeps costs low to help more businesses.

5. How do I get a loan under the credit guarantee fund scheme?

To join the credit guarantee fund scheme, visit a bank like SBI or HDFC with your ID, business proof, and a plan. Fill out their form, and the credit guarantee fund trust for micro and small enterprises checks it. If approved, you get the money fast.

Reference: https://www.cgtmse.in/

DISCLAIMER:

The information provided in this document regarding government schemes such as CGTMSE, PMFME, and PMEGP has been compiled from publicly available sources and is intended solely for general awareness, academic, and study purposes. While due care has been taken to ensure accuracy, the details of benefits, eligibility criteria, scheme duration, and related provisions are subject to change as per updates issued by the concerned ministries, nodal agencies, or implementing authorities.

Readers are strongly advised to verify the latest and official information directly from the respective scheme portals, official notifications, or authorized government sources before making any decisions, applications, or commitments. Neither the author nor the publisher of this document shall be liable or responsible for any discrepancies, outdated information, or subsequent changes, including modifications, extensions, or withdrawal of the schemes